When it comes to tracking my personal finances, I’m wary of financial aggregators like Mint and Personal Capital. I don’t want all my financial data in one place. Have you seen all the data breaches lately? For that reason I use google sheets to manage my finances. Admittedly Mint does track my credit card transactions, simply because I’m not actually sharing my password with Mint. I only use Chase credit cards, and Chase and Intuit (Mint) have an Oauth agreement.

The google sheets workbook I created is made up of various spreadsheets. In one, arguably most important, sheet, I input my daily transactions and categorize them. This data is used for calculations in separate tabs throughout the document. I only do this once or twice a week, since mint captures 99% of my transactions except for cash/debits/ACH payments. Below is a glimpse of some entries:

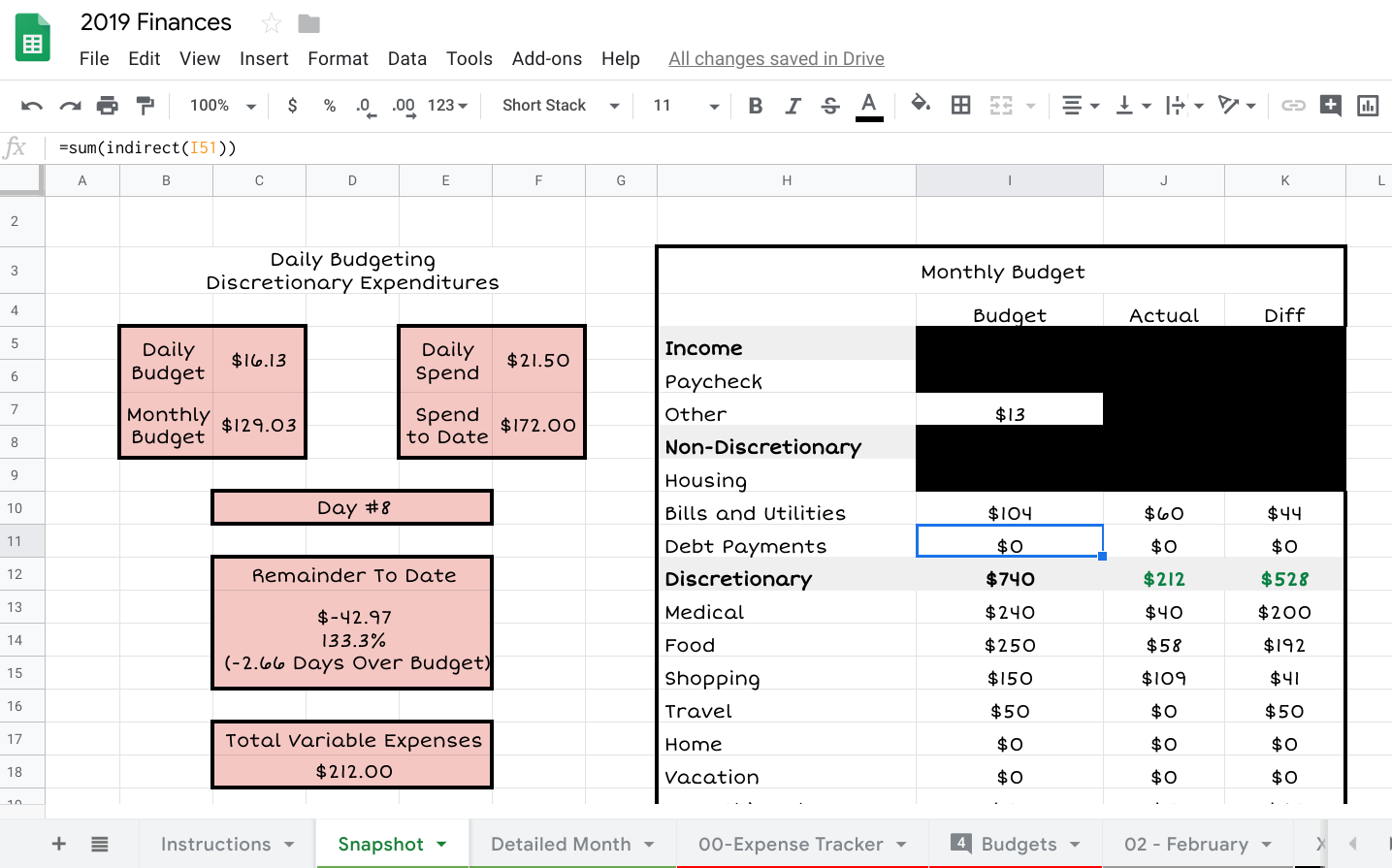

The information from this spreadsheet is pulled and used to provide a month-to-date snapshot of my income and spending:

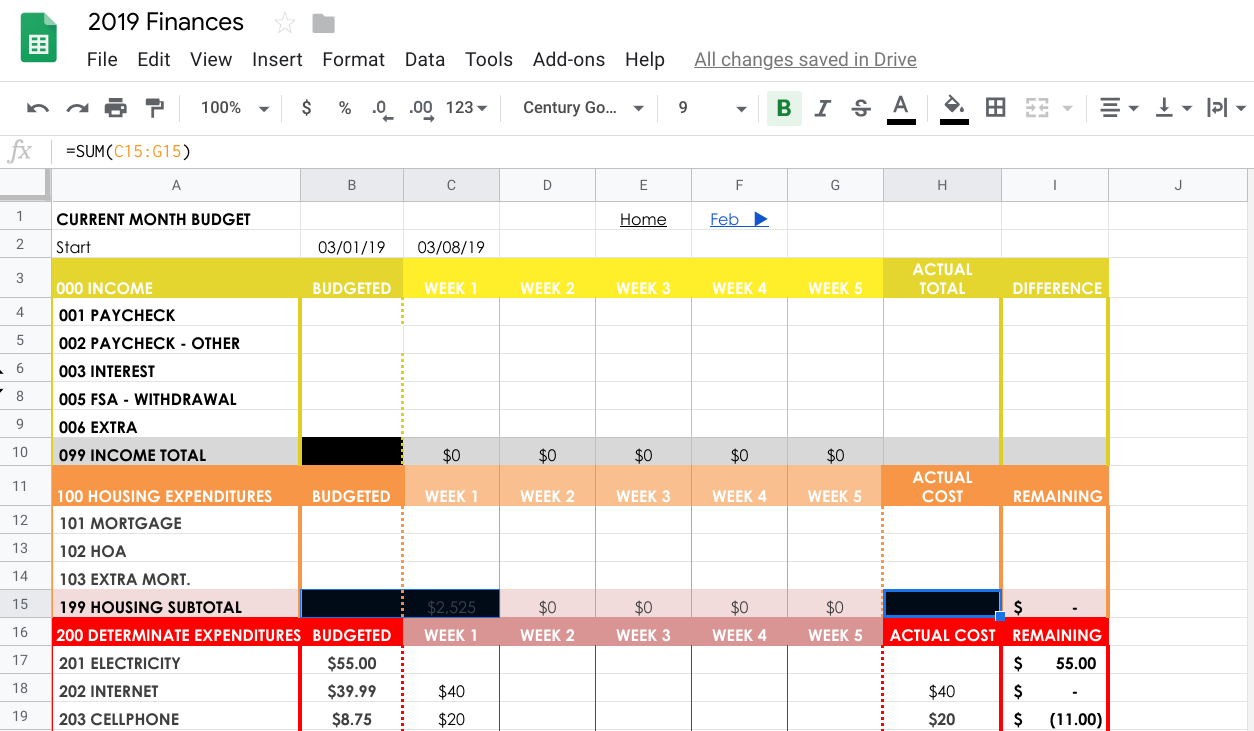

Within this document, I spend 95% of the time inputting my daily transactions and/or visualizing a snapshot of my spending-to-date. But, as stated, I do maintain other tabs as well. For instance, there is a more detailed month-to-date sheet that I rarely look at:

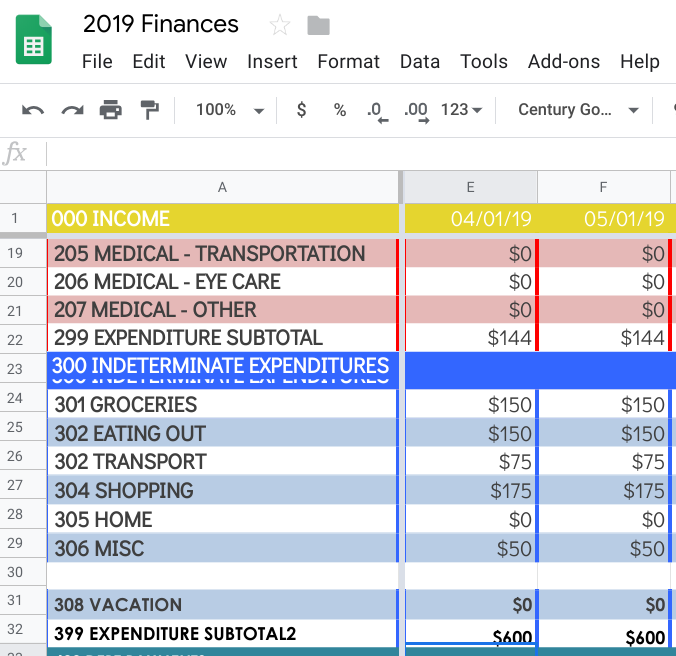

I use another sheet to track my net worth. I only update this at the end of the month though (A similar sheet tracks my YTD spending, but this is update automatically):

For the most part, I try to stick to the same budget from month to month, but if I need to change it, that can be done here:

Other notable features in this particular financial workbook include:

- Instructions on how to use the document & make changes

- Historical detailed monthly budgets

- A paycheck calculator

- Charts and graphs galore

- Income tax calculator

- Investment tracking

- Projections