In May I got a sizable promotion, and decided to celebrate by splurging. I threw caution to the wind and didn’t follow a budget. I also had two additional sources of unexpected income, and that made the decision to splurge a lot easier.

While this promotion did result in a sizable increase in income, the promotion means so much more than money. Working will likely always be difficult for me. Most days I do not feel well due to a chronic illness that I have. I’m happy that I still, somehow, manage to perform well at work

Anyways, my net worth!!

| Liquid Assets |

Start |

End |

$ Change |

| Cash & Checking |

$1,585 |

$1.085 |

($500) |

| Emergency Fund |

$4,338 |

$4,575 |

+$237 |

| Savings Goals |

$284 |

$365 |

($81) |

| Brokerage Accts |

$898 |

$1,080 |

($182) |

| Illiquid Assets |

Start |

End |

$ Change |

| Savings Bonds |

$1,704 |

$1,603 |

($101) |

| Home Equity |

$15,368 |

$16,000 |

+$632 |

| 401K |

$30,234 |

$31,760 |

+$1,526 |

| Roth IRA |

$22,079 |

$22,641 |

+$562 |

| Liabilities |

Start |

End |

$ Change |

| Credit Cards |

($1,006) |

($342) |

+$665 |

| Loans |

($17,713) |

($17,368) |

+$345 |

| Net Worth |

$57,771 |

$61,400 |

+$3,629 |

| % Change |

+6.3% |

My net worth increased by 6% which is pretty decent. I think the performance of the stock markets explains most of the increase.

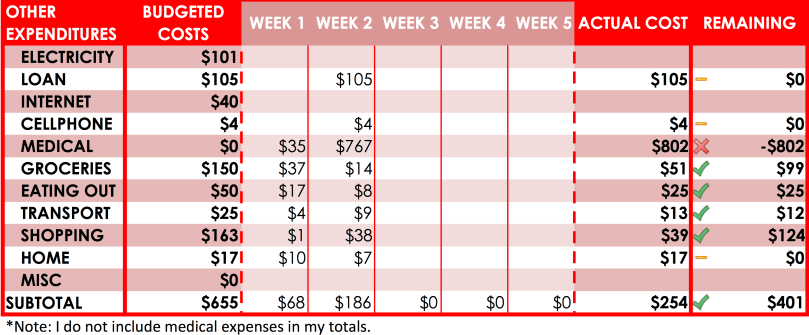

Budget & Spending

My promotion officially kicked in the second half of May, resulting in more to spend. I also had other financial good fortune. I’ve since changed my pay allotments so that the entire increase in income goes towards my 401K loan. Below is my spending for the month, I went $776 over budget:

| Category |

Budgeted |

Actual |

Remaining |

| (1) Extra Income |

$- |

$1,000 |

$- |

| (2) Bills & Utilities* |

$350 |

$349 |

$1 under |

| (3) Food |

$200 |

$205 |

$5 over |

| (4) Medical |

$- |

$262 |

$- |

| (5) Everything Else |

$200 |

$972 |

$772 over |

| Total (2+3+5) |

$650 |

$1,426 |

$776 over |

*- I increased my bill budget by $100 to prepay for next year’s amazon prime. The $100 came out of my sinking fund for semi-annual bills.

Even though it was fun to go on a spending spree, sinking funds would have made for a better financial strategy. Of the $776 “splurge”, $600 went to furniture purchases, $100 to clothing purchases, and the remainder to Ubers & Lyfts. I should have saved for the furniture and clothing, as these expenses happen eventually, just not every month. I’ve now established the following sinking funds and no longer have the more aggregate “Short-term” and “Long-term” sinking funds:

(1) Bills

(2) Personal Loan Repayment

(3) Gadgets

(4) Travel

(5) Clothes

(6) Home Goods

(7) Fun Money

Below are my budgets. Because I do not disclose my housing costs, I’ll use the following symbol to represent my original (pre-June) Mortgage & HOA payments: 🏠. This table is more for me than anyone else, but hopefully this makes sense to readers. Note, my income remains unchanged because 100% of my salary increase is going towards my 401K loan.

|

Old Budget |

June Budget |

New Budget |

| Income |

🏠 + $1340 |

(1.5 × 🏠) + $2010 |

🏠 + $1340 |

| Loan Payments |

– |

0.125 × 🏠 + 275 |

– |

| Housing |

🏠 |

🏠 – $75 |

🏠 – $75 |

| Bills & Utilities |

250 |

275 |

275 |

| Food |

200 |

300 |

300 |

| Everything Else |

200 |

300 |

300 |

| Roth IRA |

460 |

460 |

460 |

| Emergency Fund |

100 |

(0.25 × 🏠) |

|

| Sinking Funds |

130 |

(0.125 × 🏠) + $475 |

|

New vs Old

My mortgage & HOA payments will decrease by $75 starting June 1st. I’ll be increasing my “Bill & Utilities” budget by $25, my food budget by $100, and “Everything Else” by $100. The $600 budgeted for Food and Everything Else will make it easier for me to follow the $20/day budget method. Any money left over at the end of the month will likely go into a sinking fund.

June vs Old

In June I’ll be receiving 3 paychecks. My third paycheck will be going towards my personal loan, my emergency fund and my sinking funds.

Coming up in June

June should be interesting. If the stock markets hold steady, I expect my net worth to increase by well over $4,000. I will be having a minor surgery though. Hopefully those costs aren’t too high.